Open USD - Splitting the Stablecoin Float With Its Distributors

The Reserve Model, Partner Economics, and CRCL's Selloff Behind a 140-Firm Stablecoin

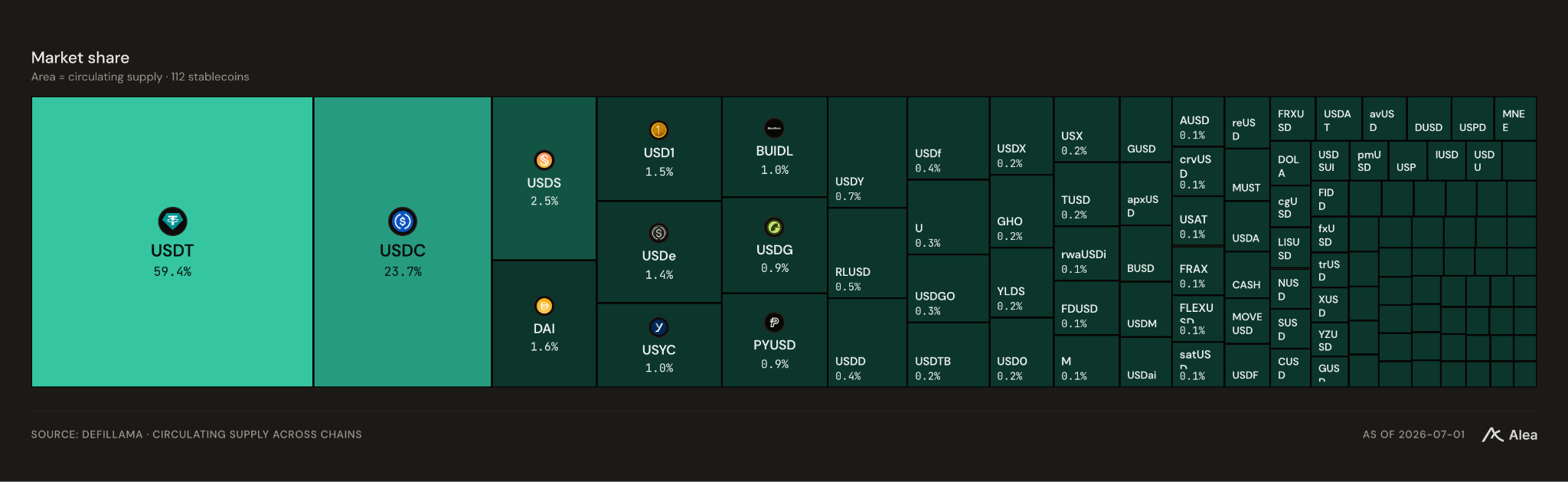

Stablecoins have been a duopoly for years. USDT owns offshore liquidity, USDC owns the US regulated market, and together they hold roughly 83% of all circulating supply. That concentration turned Tether and Circle into two of the most profitable businesses in crypto, because whoever issues the coin keeps the interest on the reserves.

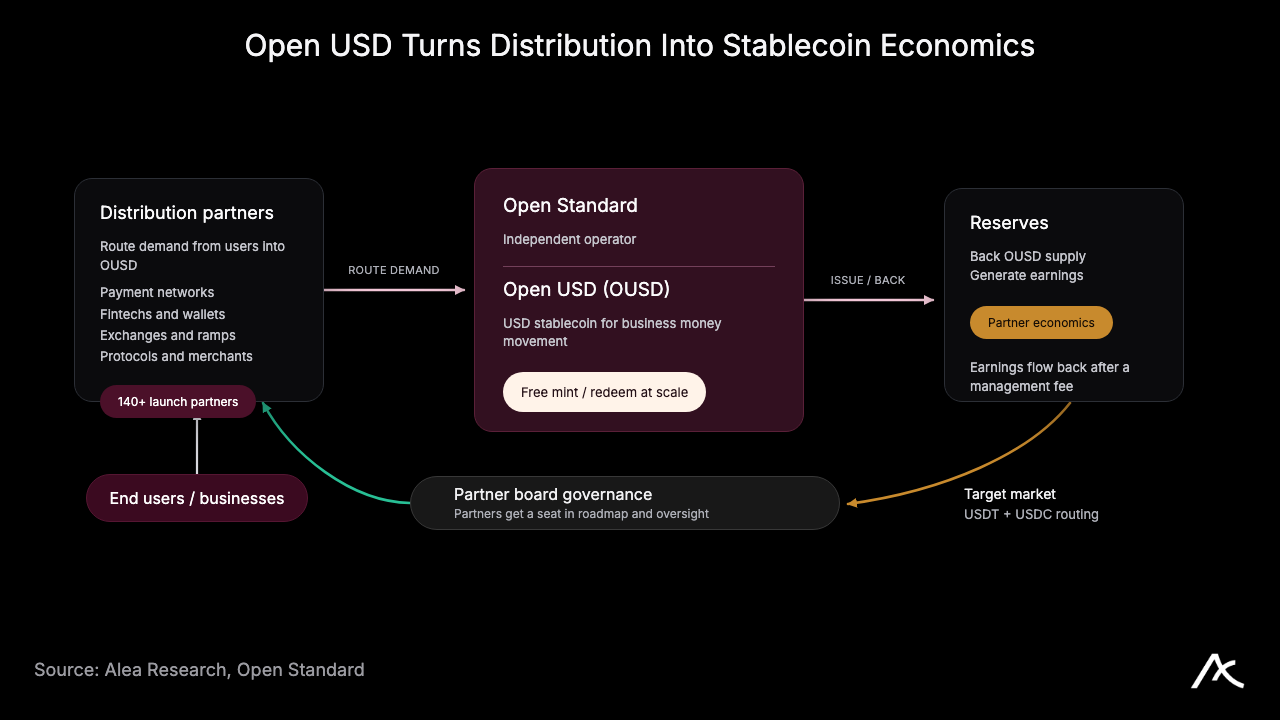

Open USD, announced on 30 June by a consortium of more than 140 companies, challenges that by handing most of the reserve income back to the businesses that route the balances.

In this edition, we look at the model OUSD targets, how its economics work, and CRCL’s selloff.

What OUSD is Transforming

The incumbent model issues the coin, holds the reserves in short-term Treasuries, and keeps the interest. At current rates that spread is the whole business. Tether reported $1.04B in net profit in Q1 2026 on just under $192B in assets, and Circle earned $653M in reserve income last quarter, about 94% of its revenue.

Payment networks, exchanges, wallets, and merchants increasingly decide what gets surfaced, held, and moved. They generate the demand that fills the reserves, yet they capture none of the yield on it. Open USD’s argument is that the party routing the balances should share in the economics it creates.

What OUSD Offers

Open Standard announced OUSD on 30 June, with a launch planned later in 2026, native to Solana first. An independent company runs it, with a board drawn from its partners, closer to how Visa or Mastercard is governed than to a single-issuer coin. Zach Abrams, co-founder of the Stripe-owned stablecoin firm Bridge, is founding CEO, which gives the venture payments-infrastructure pedigree rather than a pure crypto pitch.

Firstly, partners can mint and redeem OUSD at no cost and with no volume caps, removing a constant small leak in high-volume workflows. Secondly, partners get to keep most of the reserve earnings after a management fee, so a company routing balances earns on that float instead of handing it to the issuer. And lastly, the partner board holds governance, giving distributors a say in the coin’s direction.

More than 140 companies signed on at announcement, among them Visa, Mastercard, Stripe, BlackRock, BNY, Google, Shopify, Coinbase, and Ripple.

This creates a self-reinforcing loop where partners route balances, supply grows, reserves earn, partners get paid, and the payout gives them a reason to route more. The loop only holds if the split feels fair, but the split has not yet been explicitly defined.

The Opportunity Pool

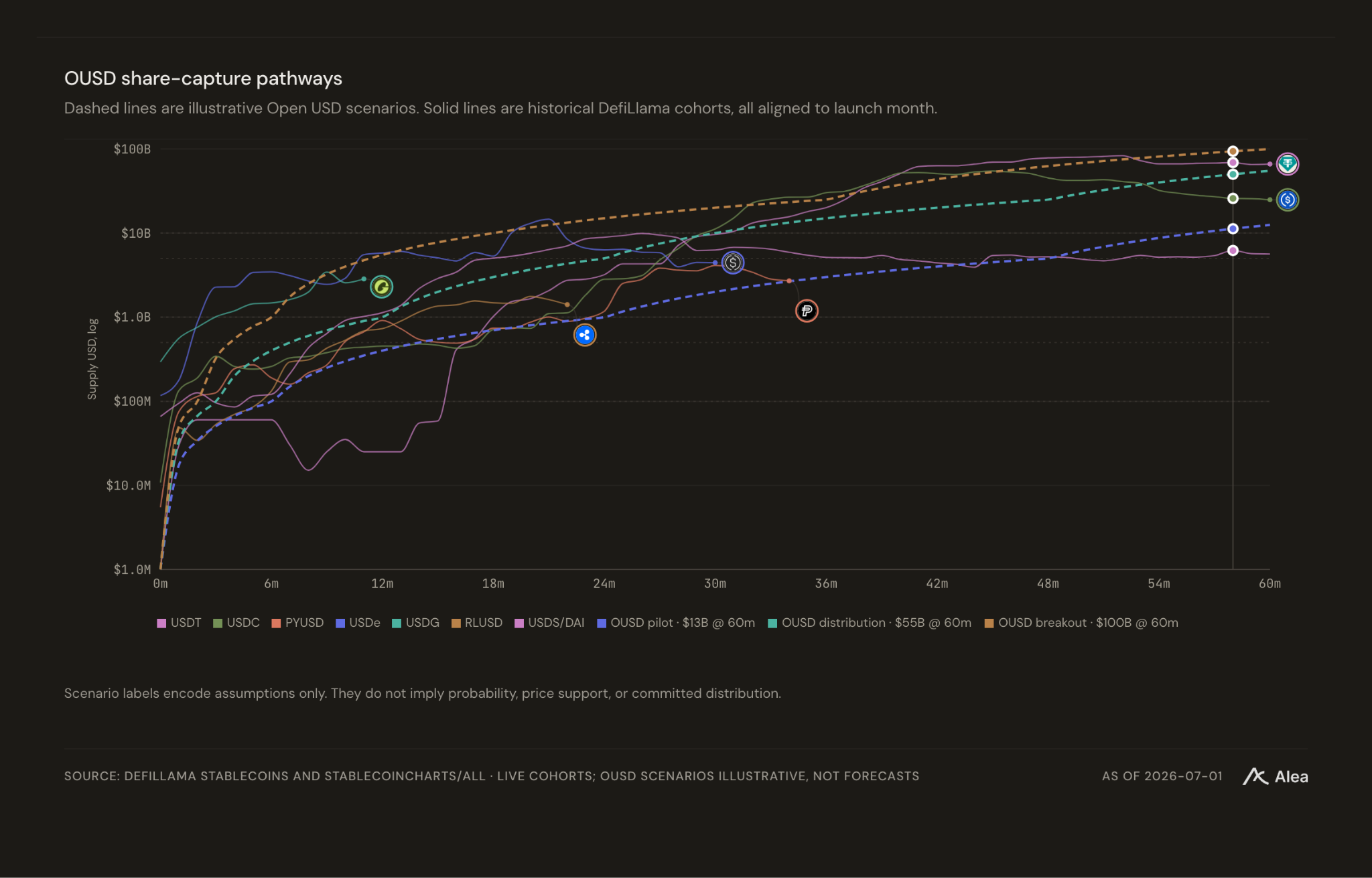

Circle earned $653M in reserve income on about $77B of USDC last quarter, which points to an annual reserve yield near 3.5%. At that rate, every $10B of OUSD balances throws off about $350M in gross annual reserve income before fees, and matching Tether’s current $184B would generate roughly $6.4B a year.

At scale, the float is large enough that partners have a good economic incentive to route into it. Whether the allocation stays wide enough to keep both giants and small partners engaged is the open question.

CRCL -17.5% Reaction

Circle is public, so its stock became a proxy for pricing the threat. CRCL fell 17.5% on 30 June to close near $65, a four-month low, on a coin with no supply, no redemptions, and no liquidity yet.

Paxos’s partner-owned, revenue-sharing Global Dollar (USDG) launched in late 2024 on the same premise and has reached only about $3B, against USDC’s $73B and USDT’s $184B.

Circle is not a weak business, ending Q1 with $77B of USDC and $21.5T in quarterly onchain volume, and its CEO publicly defended USDC’s network effects after the drop.

Tether is harder still to dislodge, with an edge in liquidity, habit, and trading-pair depth. The move is a read-through on where float economics could migrate, not proof that any has.

Coinbase’s Hedge

Coinbase is both Circle’s largest USDC partner and now an OUSD partner. This has been picked up by many as a threat to Coinbase and Circle’s partnership.

Circle’s filings show Coinbase earns 100% of the reserve income on USDC held in its own products and 50% on USDC held elsewhere, plus a minority equity stake in Circle. Stablecoin revenue was about 23% of Coinbase’s net revenue in Q1 2026, roughly $305M of $1.34B.

Joining OUSD seems to be a hedge rather than defection. Coinbase can keep earning on USDC while securing a seat in any model where distribution captures more of the economics. That is not evidence it is leaving USDC, especially pre-launch. It is evidence Coinbase sees where the leverage may move.

What Has to Happen Post-launch

OUSD enters as the challenger in a duopoly market without any proof of traction yet. Its roster makes it credible, but also raises the cost of failing to deliver, because 140 marquee partners lending their logos puts their reputation on the table.

The vision can work only if the whole partner cluster realizes its potential. It’s them who need to route balances, make OUSD a default, and treat the shared earnings as real revenue. Bring stablecoin flow, earn part of the float.

The speed at which it reaches USDC and USDT scale depends on the payout model, since that’s the core value proposition for partners. Paying partners to scale OUSD gives them a clear reason to move more balances into it.

Important Links

Become a Premium member and get the full Alea platform.

Join thousands of sharp crypto investors & traders using Alea to evaluate opportunities and deploy with conviction. For just $149/month, Premium unlocks:

Full report suite: Deep Dives, Perspectives, Blueprints, Theses, Benchmarks, Memos & Pulse.

Protocol Data Rooms: Standardized due diligence portals with live analytics, risk matrices, and governance tracking across 24+ protocols.

Podcast Digest & Summit Digest: Key takeaways from the conversations shaping markets, so you don’t have to listen to every pod.

Governance Tracker: Live proposal feeds and voting activity across major protocols.

Full access to the historical research archive.